top of page

2026 Tax Litigation Report

First-tier Tax Tribunal

First-tier Tax Tribunal

- FTT substantive decisions

The basic approach was to seek to separate the decisions between (1) decisions on substantive tax issues; (2) procedural issues; (3) penalty appeals; and (4) applications to admit late appeals. Substantive tax decisions that also involved penalties were generally placed solely in the substantive tax issue group.

Coronavirus Job Retention Scheme and High Income Child Benefit Charge decisions were excluded.

In terms of identifying the successful party in each case, there were three options: (1) taxpayer (T) win; (2) HMRC win; (3) mixed. Allocating cases obviously involved elements of judgment, particularly where the overall result was technically "mixed" but one party's success was limited (or perhaps the result of HMRC consenting to an assessment being reduced). The difference between total taxpayer wins and total HMRC wins for a category is the mixed results.

Some cases involved multiple taxes and were grouped based on which tax seemed to be the most important.

The source for the decisions was Bailii. Whilst significant time was invested (here and throughout), it cannot be guaranteed that the figures are in all respects wholly accurate.

Necessarily, there is an unknown number of "summary decisions" which the FTT does not publish and, therefore, the results of which cannot be factored in.

- FTT substantive decisions

- FTT representatives (in substantive decisions)

This table is based on who represented each party in each of the substantive decisions. Where a party had multiple representatives, only the first named was counted. Some decisions were made on the papers and are not included.

For the taxpayer, there were four possibilities: (1) Counsel (KC); (2) Counsel (non-KC); (3) Non-Counsel representative; and (4) In person.

For HMRC, there were three possibilities: (1) Counsel (KC); (2) Counsel (non-KC); (3) Litigator.

In cases where the taxpayer was represented by a KC, HMRC were represented by a KC about half the time in 2024 (45%) and nearly one third of the time in 2025 (27%). In contrast, in cases where HMRC were represented by a KC, the taxpayer was represented by a KC in all except one case in 2024 and three cases in 2025.

- FTT representatives (in substantive decisions)

- FTT procedural and late appeal decisions

This table includes (1) late appeal decisions; and (2) procedural decisions. Procedural decisions covered a wide range of issues with it not being unusual to have more than one issue determined in each decision. For some procedural issues with sufficiently large numbers, the figures are also provided independently.

In relation to appeals against information notices, the most common result was that the information notice was adjusted in some way.

- FTT procedural and late appeal decisions

- FTT penalty decisions

These are, in general, the appeals the concerned only an appeal against a penalty (penalty appeals mixed with substantive issues were generally only included in the substantive table. For some types of penalty with larger numbers, the figures are also provided independently.

- FTT penalty decisions

Upper Tribunal

Upper Tribunal

- UT decisions

This table seeks to represent the overall results in UT decision in the two years considered. The methodology was similar to the FTT.

It also shows, where there was an FTT decision, the broad effect of the UT decision on the FTT decision. Not all decisions relate to an FTT appeal, given that the UT heard judicial review claims.

The Appellant success column seeks to show whether the party who was appealing (or the main party appealing) was successful or not.

High Court Judges were part of the panel deciding the UT case in approximately 42% of cases in 2024 and 43% of cases in 2025.

- UT decisions

- UT decisions by tax

This table shows the combined results for each tax/category for the 2024 and 2025 years combined (to give a bigger data set).

- UT decisions by tax

Court of Appeal

Court of Appeal

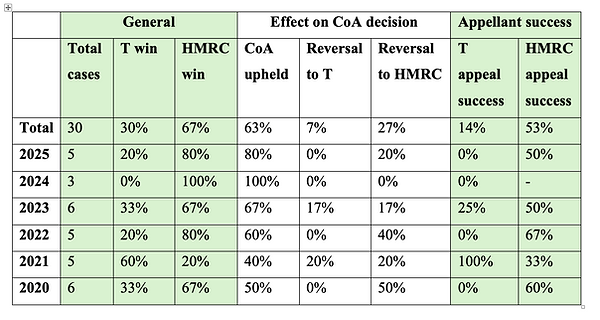

- Court of Appeal decisions

This table shows the Court of Appeal tax decisions going back 5 years, to give a bigger data set. The approach and presentation is the same as for the UT.

- Court of Appeal decisions

- Court of Appeal by tax

This table shows the combined results in the Court of Appeal, by tax, for the five years from 2021 to 2025.

- Court of Appeal by tax

Supreme Court

Supreme Court

- Supreme Court decisions

This table shows Supreme Court tax decisions going back to 2020. The smaller data set made it possible to go back further. The approach and presentation is the same as for the Court of Appeal.

- Supreme Court decisions

- Supreme Court decisions by tax

This table shows the combined results, in the Supreme Court, by tax for the years 2020 to 2025.

- Supreme Court decisions by tax

Specific taxes

For certain taxes with a significant number of decisions at each appellate level, the data has been combined to see results at each stage.

Specific taxes

- VAT

This table combines the data for each appellate level above into a single table to show the overall results at each level. Note that the data ranges are different at each level, reflecting the greater volume of cases that would need to be analysed.

There was no overall win by taxpayers in CoA and UKSC in any VAT case between 2022 and 2025 (inclusive).

- VAT

- Income tax

This table follows the same approach as for VAT.

- Income tax

- Employment tax

This table follows the same approach as for VAT.

- Employment tax

- Corporation tax

This table follows the same approach as for VAT.

- Corporation tax

bottom of page